Will Carbon Fiber Find Widespread Use in the Automotive Industry?

Carbon-fiber composites (also called carbon-fiber reinforced plastics or CFRP) are finding their way into new applications as industries demand materials with ever-higher strength-to-weight ratios, corrosion resistance, and workability. Over the past 60 years, CFRPs have been increasingly used to replace metal in applications where light weight has outsized value (capable of supporting prices that can reach $140/lb), primarily for reducing fuel consumption.

CFRPs face a divided path: well established in high-value sectors such as sporting goods, aerospace, military, and supercars, but priced out of most large-volume markets, particularly the mainstream automotive industries. This will continue until emerging methods and materials speed up CRFP production and bring down the high prices.

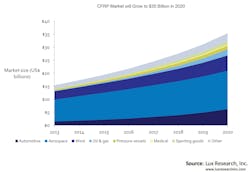

In 2020, CFRPs across all applications will comprise a $35 billion market, including $6 billion in automotive CFRPs, according to Lux Research. However, that automotive use will be limited to luxury and racing vehicles. Analyses indicate that large-scale, mainstream CFRP automotive adoption before 2020 is unlikely. But sometime after 2020, the potential volume of CRFP used in cars and trucks could dwarf all other applications, potentially reaching hundreds of billions of dollars.

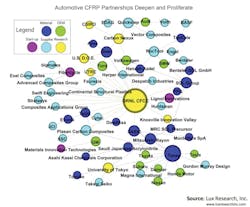

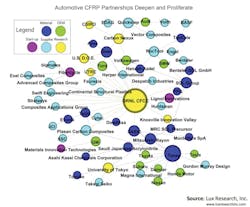

As a result, most major automotive companies and carbon-fiber producers are forming partnerships, joining consortia, and conducting research to bring automotive CFRPs closer to commercial reality. Oak Ridge National Laboratory’s (ORNL) Carbon Fiber Composites Consortium remains the most connected entity on the automotive partnership map, with 23 OEM, Tier 1, and major material supplier partners. ORNL’s Carbon Fiber Technology Facility, a 25-ton/yr. pilot carbon-fiber production line is exploring methods of making fiber at lower costs. The facility demonstrated two years ago that it can turn out standard modulus carbon fibers—with tensile strengths of 500 ksi and modulus as high as 36 Msi—using textile-grade polyacrylonitrile (PAN) precursor. ORNL says it costs less than one half as much as fiber-grade PAN.

Today, ORNL faces competition from Carbon Nexusan’s 20 ton/yr. pilot production line established by Australia’s Victorian Centre of Advanced Materials Manufacturing. Carbon Nexusan, partnering with Dow, Quickstep, Volkswagen, and Australian national research agency CSIRO, is developing its own alternative precursor, tensile strength improvements, and energy-efficient technologies, many of which could be used with ORNL’s methods. In addition to advances in fiber production, suppliers throughout the value chain are developing faster, more efficient equipment, resins designed for automotive CFRP use, and scalable CFRP recycling methods.

Among auto companies, BMW stands out as a pioneer of CFRP use. It first invested in carbon-fiber maker SGL in 2009, a relationship that continues with BMW investing $200 million more just last year to push production capacity from 6,000 tons to 9,000 tons/yr. BMW will use the materials in its i-Series electric and plug-in hybrid cars, which are currently rolling off production lines at a rate of 100 cars per day.

More recently, BMW has partnered with Boeing, a world leader in using CFRPs for aerospace manufacturing. The two hope to improve CFRP production and recycling. By leveraging both upstream fiber capacity investment and the knowledge of experienced players like Boeing, BMW is positioning itself to lead the way in large-scale automotive CFRP manufacturing.

Still, the future remains uncertain. Development trends underway in fiber, resin, and composite part production strongly suggest that by the mid-2020s it will be technically and economically feasible for automotive OEMs to make mainstream vehicles that use significant amounts of CFRPs. However, CFRP technology is not the only determinant for whether, when, how, and how much CFRPs will actually be used in cars and trucks. Additional factors inside and outside the industry will strongly affect the pace and penetration. Fundamentally, the push toward automotive composites is predicated on the idea that reducing weight is a cost-efficient method for reducing fuel consumption. (A 10% reduction in weight typically leads to 6% to 8% reduction in fuel consumption.) As a result, vehicles will gradually become lighter as fuel economy standards become stricter. Meanwhile, CFRPs—the materials with the highest specific strength—will be waiting to be used when they get cheaper.

In electric vehicles, such as the BMW i-series, the payoff for reducing weight is even greater due to secondary cost savings from using smaller, lighter batteries. However, alternative methods of reducing gasoline use such as hybridization and using alternative fuels like natural gas, hydrogen, and biofuels, are gradually becoming less costly as their underlying technologies continue to advance. As a result, the idea of a fixed cost at which CFRPs can be adopted must be understood relative to current vehicle designs. By the time CFRPs are inexpensive enough to adopt, the goalposts may have moved, as the price might still not yet be low enough to warrant widespread adoption at that time.

In the long term, megatrend-driven shifts may further reduce the incentive to develop CFRPs for the automotive industry. For example, as global population becomes more urbanized, using cars for personal transportation in the developed world may decrease as people shift to other ways to get around. In addition, individual trips taken in cars will be shorter and undertaken at lower speeds using smaller vehicles. Smaller vehicles are already lighter and more efficient, reducing the value of more lightweight materials. Indeed, some emerging concepts for urban cars are extremely light and do not resemble current passenger vehicles at all. Increasing connectivity could further the trend towards fewer personal cars and trips by car, as it will likely increase telecommuting and online shopping for goods and services, as well. As a result, urbanization might reduce the need for lightweight materials, including CFRPs, in personal transportation.

Current trends still strongly indicate significant automotive adoption of CFRPs in the mid-2020s, and companies throughout the value chain must position themselves to take advantage of the coming shifts. However, those developing these technologies should consider that there could be a limited long-term window for penetrating the automotive industry.

About the Author

Anthony Vicari

Advanced Materials team member

Anthony Vicari is a member of the Advanced Materials team at Lux Research where he covers technological and market developments in emerging materials and manufacturing technologies, including composites, coatings, and metals. He also covers longer-term, potentially disruptive innovations such as metamaterials, smart materials, additive manufacturing, and graphene. Prior to joining Lux Research, Anthony was a R&D Scientist at InnovX Systems, developing improved elemental analysis for handheld x-ray fluorescence spectrometers. Anthony earned an M.S. in Materials Science and Engineering from Carnegie Mellon University, and a B.A. (magna cum laude) in Physics and Chemistry from Harvard University.

Voice Your Opinion!

To join the conversation, and become an exclusive member of Machine Design, create an account today!

Leaders relevant to this article: